DIY Credit Repair: How to Fix Your Credit by Yourself?

DIY Credit Repair: How to Fix Your Credit by Yourself?

Published by: Ricky Ingram

Disclaimer: We provide free content for our users. But, we can earn commissions when you click on affiliate links to one or more of our advertisers. Learn more about how we make money.

The Federal Trade Commission estimates that 1 in 5 people has material errors in their reports. These are mistakes that impact scores and may disqualify you during the loan approval process.

DIY credit repair entails trying to clean up reports without the help of paid credit repair services. It’s a viable option for people who want to save on fees. Performing credit repair yourself is possible thanks to the Fair Credit Reporting Act. It gives every person the right to ensure that the information CRAs are supplying about them is accurate.

For first-timers, the process can seem daunting. Fortunately, it’s quite easy to learn how to repair credit for free. You can even achieve the same results as professionals because they use the same processes in the Fair Credit Reporting Act.

DIY credit repair has its appealing qualities. From an individual standpoint, it may boost your problem-solving skills and contribute to personal growth. Becoming an expert on credit repair strategies is a skill that will be invaluable for the rest of your life. It can even mean helping close friends and family members with their credit issues.

DIY credit repair also translates into saving on monthly fees. On average, customers pay $79 for credit repair and stay with companies for six months. Assuming you subscribe for three months, you need to pay $79 (initial setup fees) + $237 (for 3-month subscriptions), bringing the total to $316. Six months of service would cost $553.

The savings can pay down debts or serve as security for new credit rebuilding products such as secured personal loans. Here are the DIY steps to credit repair:

Step 1: Order credit reports from the major credit bureaus

When working with a credit repair company, the first step they take is checking reports for errors. They rely on paid third-party partners and later pass on the fees as part of initial costs.

It’s possible to get free reports from Annualreportcredit.com. Customers receive one free report from each credit bureau through the website. Currently, they are issuing free weekly reports as part of the COVID-19 initiative. Other places to order free reports include:

When repairing your credit yourself, you may exhaust all the free places to order reports. There is no need to wait until you become eligible to receive free credit reports again.

Consider using paid credit monitoring services offered by CRBs or third-party providers. For instance, TransUnion states that their credit monitoring service serves as a “personal assistant and watchdog.” Members are entitled to access their reports anytime, and it also offers credit protection and sends out alerts about new accounts, credit card balance increases, and more.

Third-party websites provide credit reports from all the credit bureaus, score updates, ID protection, and identity monitoring. One such service is myfico.com, which is the consumer division branch of FICO Inc.

Step 2: Check the reports for potential dispute candidates

The second step in do-it-yourself credit repair entails evaluating reports to find dispute candidates, which are inaccurate or unfair entries.

Many mistakes arise when furnishers report the wrong information to CRBs. For instance, a paid-in-full account may be reported as settled. Settled accounts can harm scores because they indicate that the borrower hasn’t paid the full amount.

Creditors often don’t have incentives to supply the most accurate information. Credit card companies are notorious for failing to report all the details about credit limits or outstanding balances. Incomplete information on revolving accounts may increase your credit utilization rate, which contributes up to 30% of the FICO score.

Check your payment history for late payment entries even if you pay all accounts on time. Sometimes creditors make mistakes by applying payments made to your account to another account.

Clerical workers may make errors when digitizing details from handwritten credit application forms. They may enter wrong addresses or personal identifiable information.

You may also be the victim of fraud resulting from the Equifax breach, where 143 million American credit files were hacked. Scammers may also steal your identity using other ways. Hard inquiries that you never made may be the first indication of fraud.

Sometimes, there are cases of mistaken identity, where sharing similar names with someone else may result in their credit history ending in your reports. Collection accounts may have errors that stem from mistakes made in the billing process. For instance, NerdWallet Health estimated that more than half of medical bills might have errors.

For a much smoother process, review each account entry in the reports using past account statements from the bank or credit card company. Credit reports also use special status color codes to mark negative items. They may use green to show that an account is okay and red to indicate a problem.

Step 3: Dispute incorrect information via mail or online

The FCRA states that customers may dispute information by submitting disputes to the CRAs or directly to credit furnishers.

CRAs provide two main ways of submitting disputes, mailing letters or using online dispute centers. For a faster process, credit repair companies use an electronic dispute system that’s more efficient than sending credit cleaning letters.

Critics of online disputes claim that they are not as effective as mailing letters. They also state that customers waiver their rights by using online dispute systems. Some services even sell “effective 609 letters” that may demand information that CRAs can’t provide, such as copies of cashed checks.

Experian has come out strongly against paid 609 letters, stating that there is no evidence that they are more effective than other ways of disputing negative information. As long as an entry is incorrect and unverifiable, it will be removed.

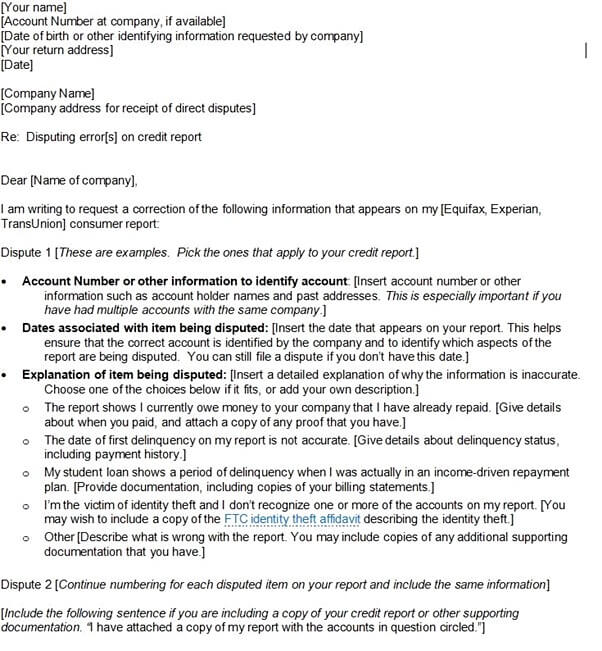

Now, if you still want to mail letters, it’s perfectly fine. For free credit repair, FTC provides a sample of a dispute letter to send to the CRBs.

TransUnion, Equifax, and Experian provide sample dispute forms specific to their platforms:

It’s good practice to include copies of supporting documents with each dispute.

Step 4: Contact the information furnisher

After filing a dispute with the CRBs, experts also recommend reaching out to the company that reported the error. The notice may entail writing a 623 dispute letter.

Consumerfinance.gov provides a sample letter to use when disputing information with the furnisher (direct download).

The CFPB also provides more instructions for disputing information with furnishers.

Creditors are also happy to help out without the need for letters. They need to protect their good reputation. So, get in touch with the customer support team and report the negative items.

Step 5: Wait it out

After initiating a dispute, the credit bureau contacts the furnisher (source of information). They request them to verify the entry in conflict. Creditors or public information sources have 30 days to respond to CRB requests.

If they confirm changes or fail to respond within 30-days, the CRB must delete the entry. At times, creditors respond after the 30-day window. That’s the reason why credit bureaus may add information they previously deleted, provided it’s true.

Step 6: Examine the results of investigations and file redisputes

The CRBs notify customers of any changes by sending an updated credit report. For instance, TransUnion will send the report using first-class US mail after 3-5 days following the completion of the investigation. If you file online, you can easily track the status of disputes.

Genuine challenges are not always successful. That’s because furnishers may not conduct an in-depth review. They may only check their computer records that may have contained the error in the first place. Some creditors may not comprehensively review the documents submitted by clients.

If the first dispute is not successful, the worst thing you can do is give up. Gather more evidence and file a redispute with the CRBs and creditors. The FCRA also allows customers to bring legal claims against the CRBs and information furnishers if all attempts to remove inaccurate negative information fail.

Alternatively, consider launching the complaint with the CFPB. It’s a U.S. government agency that protects consumers against unfair practices by lenders, banks, or other financial entities.

Consumer statements can help explain reasons for negative items. They may be handy when you disagree with the results of investigations. It can be a way of opening a new line of conversation with a potential lender, employer, or landlord as they review reports.

CRBs allow customers to add general and account specific-statements. They should not be more than 100 words. For instance, to explain a late payment, you may state, “ I fell behind my credit card payments because I lost my job amid the pandemic.”

Remember that negative items have a limited shelf-life. For instance, CRBs remove late payments after 7 years. Experian advises customers to remove statements that are not relevant anymore. If a lender encounters a statement about an account that’s already removed, they may ask about it.

Get in touch with the respective CRB support team by navigating to their websites and ask about customer statements.

Step 8: Get your updated scores

Ordering FICO score updates can help you assess where you stand following the removal of inaccurate entries. However, credit reports don’t have scores. Some places to receive free VantageScore or FICO scores include:

Step 9: Try alternative means to remove legitimate negative entries

There are two ways of having legitimate negative entries removed from reports. However, they may not have the same success rate as challenging inaccurate entries.

Consider petitioning lenders to remove recently added late payments. First, get in touch with the customer support representative. They may not have the power to remove an entry, so ask to speak to the person in charge. It’s essential to offer the right explanation. For instance, explain that a recent pay reduction resulted in a budget deficit that made it hard to pay. Alternatively, write a formal Goodwill letter.

The second method entails negotiating for Pay for Delete agreements with creditors or debt collectors. You offer to settle the debt in return for having negative items removed. While the success rate is low, it’s worth the shot. If a single late payment is deleted, it may even boost scores by up to 60 points.

Are you dealing with massive debt levels or collections accounts? They are major roadblocks to your ideal credit scores. So, let’s talk about extra tips to repair credit.

Step 10: Analyse your credit accounts and finances

Professional debt management or negotiation services first analyze your debt situation and financial profile. They then create plans to resolve the debts.

When conducting DIY credit repair, also start by determining the outstanding balances on all credit accounts. Sum all the balances to arrive at a total. Let’s say you owe $20,000 across all credit accounts. Don’t panic or worry! Take another review of your personal finances, taking stock of your income, fixed expenses, and variable expenses.

The next step is to create a budget. It should allocate money for savings. Think of ways to reduce expenses, too. You can reduce your rental expenses to allocate more money for debt payoffs or repayments. Increasing earnings can also ensure that more money is going towards paying off debts.

Step 11: Determine which debts to pay off first

Paying off debts should be done systematically by prioritizing credit card balances with the highest rates. That’s because reducing the balances on more expensive cards can translate to lower interest payments. After missing payments on credit cards, card insurers may start charging a penalty rate of up to 30%. Check if this is the case for some cards.

If you have limited funds and must decide between collections accounts or active credit accounts, keep paying the monthly payments to avoid late payment entries.

Note that paying off and closing accounts in collections will not necessarily boost scores. A paid and unpaid collections account remains on the reports for seven years and tends to have the same impact.

Step 12: Research the Statute of Limitation laws in your state

Is a debt collector threatening to sue you for debt? The “Statute of Limitation” may make a credit account uncollectible. It can be a line of defense if the creditor sues.

How does it work? Collectors can’t sue if debts are older than a specified number of years. The time period varies per state. For instance, California has an SOL of 4 years on most debts.

The countdown starts from the last day you made a payment. Making a new payment restarts the clock. Collectors will often try all possible means to keep the debt from becoming uncollectible.

Step 13: Negotiate settlements with debt collectors

Debt collection companies purchase debts for pennies on the dollar from mainstream lenders. That makes it possible to negotiate with them for a lower payment than the amount owed. If they are demanding $1,000, they may have purchased the debt for $300 and may settle for $500 and make a profit.

When repairing credit on your own, it’s possible to negotiate. There is no need to hire debt settlement companies that charge fees based on the amount they help consumers pay.

Just take the collectors calls as usual. Explain that you wish to settle for a lesser amount. They may create a lot of fuss, but they enter into such deals all the time with negotiation services.

Unfortunately, the collections industry has more bad people than good. That’s why it is essential to be careful. If they agree to a settlement, ask them to put it in writing.

Some extra credit repair tips when dealing with collectors include:

Ascertain the amount of debt owed by writing a debt validation letter;

Avoid sharing too much information about yourself as they may use it against you;

Be cautious when giving collectors access to your accounts or when setting up automatic repayments. Some companies may take out more money than agreed.

Step 14: Try various strategies to save money

Trying to save money can test your discipline. There are tips and tricks to make this process easier.

Contact your bank and ask them to set up automatic transfers from checking to savings accounts. Auto debits remove the temptation of deciding whether to save money or not.

Money-saving apps can even make saving enjoyable. Digit, a popular finance app, uses smart algorithms to make personalized recommendations. Some apps round up spare change on purchases and put it in savings or investment accounts.

The ideal goal should be saving at least 3-months worth of expenses. If unexpected life events affect your income, you can still stay current on credit payments.

Step 15: Apply for credit rebuilding products

When considering how to fix your credit yourself, apply for credit rebuilding products that allow consumers to generate positive credit entries. They may also help you adopt responsible credit habits. Two of the most popular credit building products are secured credit cards and personal installment loans.

Lenders will first require a security deposit. You can’t borrow more than the collateral, which reduces risks for the lender when issuing loans to people with bad scores.

Step 16: Obtain credit counseling for free

Although the best credit repair advice is free, consider speaking to a credit counselor. Most providers of credit counseling services are “non-profits.” They retain their status by offering a free credit counseling session. It lasts for about 30 minutes, where a credit counselor reviews your financial situation. They also recommend more credit repair options. The counselors may push their paid services, but there is no need to sign up for them.

Note about aggressive credit repair tactics

Be wary of scammy services and illegal repair techniques such as “credit sweep.” It entails lying that someone stole your identity, which prompts the CRBs to review each negative item for accuracy. Another aggressive credit repair tactic is jamming. Basically, it involves sending multiple letters to dispute the same negative entry.

Bottom Line

You now know the best way to fix your credit without any help. However, spotting errors in reports and filling out dispute forms may take a bit of time. By hiring a reputable credit repair company, you delegate the process to professionals, freeing you up to focus on other things. You can read our reviews on top repair companies like Sky Blue, Credit Saint, and Creditrepair.com.

Ricky Ingram

Founder of Credit Repair Partner. I worked in the credit repair industry for about 10 years. I love, helping people become smarter about their credit and finances.

Have you recently received a letter from LVNV Funding LLC? LVNV Funding is a debt collection agency that purchases debt from creditors all over the country and then attempts to collect it. This may be due to a past debt that you have associated with one of your credit lines. The situation can be confusing...

Has the CBC Group recently reached out to you? Or have you received a statement for outstanding medical bills, utilities, and other accounts?

Get Help With Late Payments!

(877) 324-2390

Free Consultation

If you’re currently dealing with a...

A 633 credit score is considered slightly below average and is categorized in the “fair credit score” group. Despite the fact that you are not in the poor score category, there is still so much room for growth, and you should take advantage of it. Think of your score as a stepping stone to bigger...

A 619 credit score is a fair credit score, putting you side by side with the average American. It is not a bad score, but it is also not excellent. When lenders see a 619 FICO score they will most likely not show an unwillingness to work with you, but they will end up giving you higher interest rates....

A 627 credit score is something to work on and improve as it falls into the fair credit score range. Consumers in this category may be regarded as subprime borrowers. They statistically have a higher rate of becoming delinquent than borrowers in higher credit score categories.

The impact of poor scores...

Millions of Americans struggle with their credit scores. The best credit repair software can provide you with the resources to help you in the process. Credit is not an easy topic to navigate, and making small mistakes can drastically hurt your score. When it comes to the importance of keeping a high...

Founder of Credit Repair Partner. I worked in the credit repair industry for about 10 years. I love, helping people become smarter about their credit and finances.