Disclaimer: We provide free content for our users. But, we can earn commissions when you click on affiliate links to one or more of our advertisers. Learn more about how we make money.

Credit inquiries are, at best, damaging to your credit score in the short term, and at worst, incredibly detrimental in the long term. However, if you have one of these bad marks on your account, do not abandon hope of improving your standing by removing collections from your credit report. Most of the time, it does not matter if you have a few checks in your account history. In fact, it’s normal. It only becomes an issue if you have so many that you no longer can be perceived as a trustworthy lendee.

If this is the case, then it’s possible for your score to bounce back through efforts such as removing collections from your credit report or writing a letter to dispute a hard inquiry. These actions can all be taken on your own without the assistance of professionals. If the process seems too daunting to take on alone though, there are plenty of companies that can help you out. This article will walk you through how to remove inquiries from your credit report fast. Read on to learn all about what pulls are, and what can be done about them.

Given that inquiring is defined as asking, it logically follows that credit inquiries are requests for credit. Asking for more credit is essentially asking some type of body or institution for trust. They will agree to lend you funds, and in return, you will agree to pay whatever is lent to you back — sometimes with interest. In order for an entity to determine whether it can trust you, it goes through an inquiry process.

The above process consists of reviewing your credit history for a variety of information, such as:

How long your account has existed;

How many different credit accounts you have;

How many times you have requested additional merit in the past.

This information is all collected and stored pursuant to the Fair Credit Reporting Act. If the reviewing entity finds that there is a good enough chance you will pay it back, it will usually grant your request. Inquiries in this field go by a couple of different names, such as pulls and checks. However, all three of these terms refer to the same act of analyzing you as a potential lendee.

Types of Inquiries

Inquiries are the consequence of a large variety of actions. It is important to know what they are. That way you can refrain from accidentally prompting an inquiry that you did not intend to. Pulls can be the result of:

Asking a financial institution to loan you capital to purchase a home;

Applying for a new credit card with your personal bank;

Signing up for financing when purchasing a large item, such as a car or furniture;

Responding to a credit offer you receive in the mail;

Requesting for a bump in the credit that is currently available to you;

And more!

Make sure that before you engage in any of these actions, you are informed of the potential consequences and are economically stable enough to handle them.

Hard Versus Soft Inquiries

Checks can be either soft inquiries or hard. Hard inquiries occur as a direct result of an action you are taking in an effort to obtain credit. Major credit bureaus are the ones responsible for following inquiries from your credit. They will keep them on your credit report for 24 months. Consequently, it is in your best interest to minimize the number of hard inquiries on your record at a time. When circumstances do require you to seek additional credit, it is best to strategically space out your requests so that your account doesn’t show several of them back to back.

Even if you have not heard the term soft inquiries before, you are likely more familiar with them than you think. If you’ve ever received a letter in the mail informing you that you have been pre-approved for a new card, then you have been the recipient of a soft inquiry. This means that you have not asked for additional credit, but an institution, on its own dime, has determined that if you wanted to ask for more, you could. Soft inquiries do not affect your personal credit. If they did, everyone would be in trouble!

Removing Inquiries from Your Credit Report

Soft inquiries, due to their harmless nature, are nothing to sweat about and don’t need to be removed. It’s their hard cousin that can be a cause for concern. When it comes to disputing a credit inquiry, note that not all hard pulls can be removed. Hard inquiry removal is reserved for unauthorized hard inquiries. For example, this would be the case if someone has hacked your personal information, opened an account in your name, and went on a credit shopping spree. You can monitor this activity yourself by taking advantage of your annual opportunities to review your report for free.

You cannot contest authentic hard pulls that came from your own doing. It would be a waste of your time to attempt to dispute a hard inquiry that you know was genuine.

How to Remove Hard Inquiries?

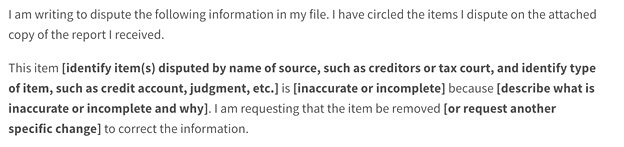

Wondering how to remove hard inquiries from your credit report? Unlike most things in the world of credit, there actually is a simple formula to follow once you have identified a removable hard pull:

Take note of the characteristics of the pull, including its date and source;

Write this information, along with an explanation of how it is mistaken, in a letter;

Submit the letter to the department of your financial institution dedicated to disputing hard credit inquiries (usually titled “dispute center” or something similar);

Monitor your pending verdict — if your argument is accepted, your institution will remove the hard inquiries you contested.

If you are unsuccessful in your attempt, it is typically for good reason. However, if the challenge you’re submitting is really a mistake, then you are not out of options. Under the FCRA, you can submit an additional statement to supplement your original one. This acts as somewhat of an appeal. Your challenge will be reconsidered taking into account any new information you provide. However, because you are given a small limit on the number of words this appeal can contain, use them wisely. Concentrate on hard evidence that the mistake is not your fault.

Deciding whether it is worthwhile to get inquiries off your credit report? Then it is important to understand the extent to which these checks can impact your standing.

FICO scores range from 350 to 800. It is in your interest to keep your score as close to 800 as possible. Hard pulls will almost always decrease your score temporarily by a couple of points. The extent of this dip will vary based on who you work with though, as many institutions have their own formulas for calculating scores. Once your challenged credit inquiries drop off, you should see an immediate improvement in your score.

Although credit reporting agencies have different methods of calculating your score, they all consider hard pulls and the time frame in which they took place. Nobody wants to discourage the practice of hunting for good deals. If you authorize a couple of different hard pulls for the same type of credit within a few days of each other (typically about two weeks), this will only count as a single pull. If on your report you notice that you have multiple hard pulls that should have been treated as only one, you can get rid of the extra hard inquiries.

Just because you have a check of a hard nature on your profile, it does not mean you have to take any action against it. In fact, most of the time, you will still be viewed as a trustworthy applicant despite having made a few pulls. Companies know that doing so is just part of everyday life. Where you can run into problems is when these pulls do not seem as though they were conducted in a responsible nature, or if they somehow indicate that you are in distress.

How Long Do Inquiries Stay on Your Credit Report?

As briefly mentioned above, you generally are stuck with your intentional checks for about 24 months. After these two trips around the sun, credit bureaus will remove them from your profile. However, just because they are on your report, it does not mean that your score will be decreased for that entire time. In fact, most hard pulls will only affect your score for half of that time — 12 months.

Thus, many people can go their entire lives without having to worry about disputing inquiries. If you would like to apply for additional credit but are in no rush to do so, it is in your best interest to wait a year after your last hard pull if your score is not otherwise high enough. If you are itching to remove your hard inquiries fast though, and feel you have the standing to do so, see the following section for steps on drafting a letter to remove inquiries from your credit report.

Sample Letter to Remove Inquiries

The Federal Trade Commission has provided sound guidance on how to write a hard inquiry removal letter. First, you should start with a heading that includes your information and the date of your submission, followed by the institution’s information and formal address.

Then, you should briefly state that you are seeking credit repair inquiry removal and specifically indicate what you believe should be removed. After that, you need to explain why you believe your request deserves to be granted. This is the most important part of your letter. If you provide an insufficient explanation or reasoning, your efforts won’t pay off.

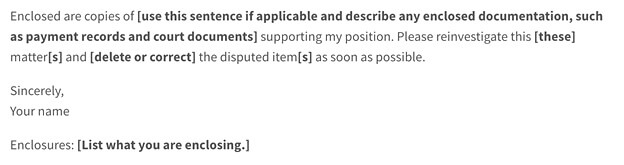

Include any documents necessary to prove your point, even if you think your institution already has access to them. The easier you make the decision for them, the better. Then, inform them that the documents are enclosed, reiterate your request to get the hard inquiries off your credit report, and sign your name.

Note that it is seldom helpful to include the hard inquiry removal time frame you are hoping for. Often, this will just annoy the employee tasked with reviewing your letter and may even make you seem less credible. Just request that the task should be done as quickly as possible.

Also, be mindful that the words you choose should be of a professional nature. It will do no good to use casual or otherwise inappropriate language. Remember that the people that will be reading what you have to say are not the ones at fault for the mistake. However, they are the ones who stand between you and what you’re seeking. Approach the situation with respect.

Should You Get Help with Removing Hard Inquiries?

If you do not feel comfortable taking the actions described in this article alone, fear not. There are financial services available that can either walk you through how to get inquiries off your credit or completely take care of it for you. If you are in a situation in which you desperately need a hard pull removed, choosing to go with a professional is your best bet.

No matter which route you decide to take, trust that it is possible to remove credit inquiries. The process just requires a bit of elbow grease. So long as you are only challenging pulls that are actually incorrect, you should not run into any problems.

Ricky Ingram

Founder of Credit Repair Partner. I worked in the credit repair industry for about 10 years. I love, helping people become smarter about their credit and finances.

Have you recently received a letter from LVNV Funding LLC? LVNV Funding is a debt collection agency that purchases debt from creditors all over the country and then attempts to collect it. This may be due to a past debt that you have associated with one of your credit lines. The situation can be confusing...

Has the CBC Group recently reached out to you? Or have you received a statement for outstanding medical bills, utilities, and other accounts?

Get Help With Late Payments!

(877) 324-2390

Free Consultation

If you’re currently dealing with a...

A 633 credit score is considered slightly below average and is categorized in the “fair credit score” group. Despite the fact that you are not in the poor score category, there is still so much room for growth, and you should take advantage of it. Think of your score as a stepping stone to bigger...

A 619 credit score is a fair credit score, putting you side by side with the average American. It is not a bad score, but it is also not excellent. When lenders see a 619 FICO score they will most likely not show an unwillingness to work with you, but they will end up giving you higher interest rates....

A 627 credit score is something to work on and improve as it falls into the fair credit score range. Consumers in this category may be regarded as subprime borrowers. They statistically have a higher rate of becoming delinquent than borrowers in higher credit score categories.

The impact of poor scores...

Millions of Americans struggle with their credit scores. The best credit repair software can provide you with the resources to help you in the process. Credit is not an easy topic to navigate, and making small mistakes can drastically hurt your score. When it comes to the importance of keeping a high...

Founder of Credit Repair Partner. I worked in the credit repair industry for about 10 years. I love, helping people become smarter about their credit and finances.