Disclaimer: We provide free content for our users. But, we can earn commissions when you click on affiliate links to one or more of our advertisers. Learn more about how we make money.

Lenders may make mistakes as they report information to CRBs. You may have been making on-time payments and still end up with late payment entries. Consumers can remove late payments from the credit report by disputing errors with CRBs or seeking help from credit repair companies.

Creditors report genuine delinquencies after 30 days. A single late payment can have devastating effects on scores, and it may remain on reports for up to seven years. Consumers may petition creditors to remove accurate entries, but the chances of this working are lower.

We will cover the top legal ways to clean late payments from credit reports. You will also find out how delinquencies affect scores. Let’s get started:

6 Ways to Remove Late Payments from Credit Reports

The method you choose to remove a late payment from a credit report may depend on whether it’s a mistake or if it’s accurate.

1. Hire a credit repair service

A credit repair company checks client reports for errors and files disputes on their behalf. They provide credit repair specialists who will review each negative item in the report to determine if it’s a potential dispute candidate. The best firms prepare and send custom disputes without relying too much on templates. Top firms also utilize electronic dispute systems to challenge errors much faster.

Bureaus may request evidence during the dispute process. Repair firms will help customers minimize mistakes as they submit evidence. Customers also track the status of disputes through online portals or apps.

Consider the company’s reputation before selecting a service to remove late payments from credit reports. Read independent and unbiased reviews, and also check how they resolve complaints on sites such as bbb.org. The services also offer free consultations. Try them out to have a better feel of their service quality.

It’s ideal to have the right expectation as you deal with paid services. They cannot challenge and remove legitimate late payments on credit accounts. A reputable service will only claim to remove reporting errors.

If you’re not comfortable paying their fees, consider DIY credit repair. You can achieve professional results too because repair companies utilize the same legal processes as individuals.

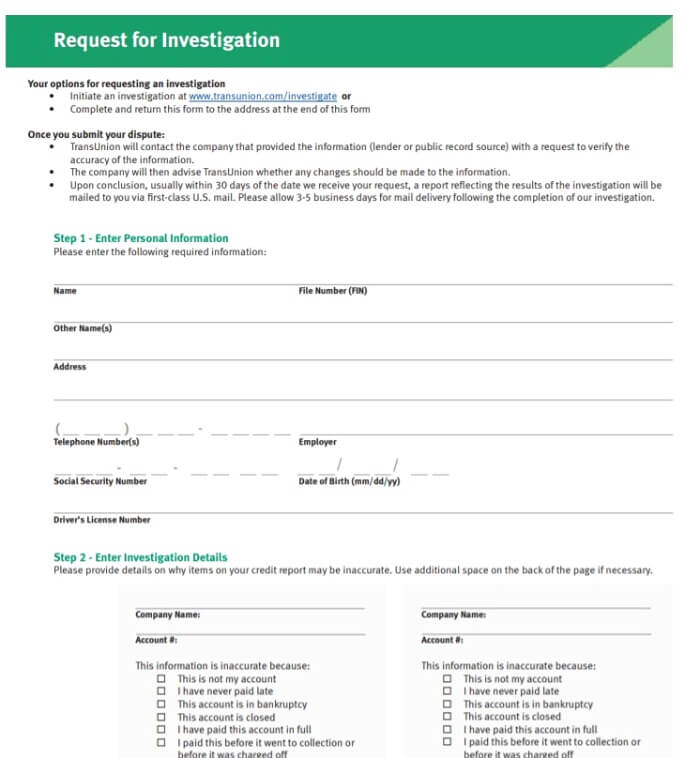

Major credit reporting bureaus must follow reasonable procedures to ensure that consumer reports are accurate. Section 611 of the Fair Credit Reporting Act provides the procedure for disputing the accuracy of reports.

You may question the accuracy or completeness of any entry by notifying the agency directly or through a reseller. After receiving the dispute, the agency will undertake a re-investigation. It’s meant to establish if the record is accurate and ascertain its current status.

The countdown to finish the investigation starts from the date they receive the notice and ends after 30 days. Credit reporting agencies may extend their investigation for another 15 days if the time is not sufficient.

How do credit bureaus get late payments removed? First, the CRA notifies the information furnisher and provides evidence submitted by the consumer. Creditors or public record resources must determine the accuracy of the dispute within 30 days.

If the furnisher reports the delinquency as inaccurate, incomplete, or fails to verify it, the reporting agency will delete the item from their files. At times, customers have entries removed only to reappear. The situation occurs if there are delays in validating disputes. Furnishers may re-insert an entry as long as it’s complete and accurate. Upon re-insertion, credit reporting bureaus must notify consumers.

If you suspect that the late payment entry resulted from identity fraud, you should notify the bureaus and ask about potential actions to take. You may place a fraud alert to tell potential lenders that you have been a victim of identity fraud or freeze your reports. The two measures prevent scammers from using your stolen ID to open new credit accounts. CRBs may also ask all furnishers to re-verify details on past and current accounts.

How to launch disputes with CRBs?

In summary, you can file disputes in the following order.

Request all copies of the credit report from the CRBs through annualcreditreport.com. The site is providing free credit reports every week as part of the Covid-19 initiative.

Review the reports for all negative information.

Select your preferred way to dispute late payment errors (by mail or online).

Gather supporting evidence to support claims.

Send the dispute.

Wait for the response.

Should you choose online or mail?

Experts recommend sending custom letters by certified mail and asking for a return receipt. Standard mail is still sufficient. The basic format of the letter should contain personal identifiable information (names, SSN, and date of birth). Remember to list your credit reporting agency file number so the CRB can easily locate your file. They will need details on the credit account, including the furnisher’s name and reason for disputes. Challenges are more successful if customers supply documentation such as payment records to verify claims.

Different CRBs may have varying requirements about how customers should write their dispute letters. Use the following resources to see what each bureau requires:

If the error appears on all reports, send the letter to the three CRBs. If it’s in one file only, the other CRBs can’t help.

TransUnion and Experian provide dispute form templates. The forms have common disputing options. All you need to do is check the case that applies to you. However, the forms may feel limiting if the case is complex and requires lots of explanation.

Launching disputes through online dispute centers is convenient and faster than writing a letter. You just need to create an account, select the relevant dispute option, upload documents, and wait for confirmation.

Online disputes are a bit controversial, with some experts claiming that they are less successful. They further state that customers waiver their rights by submitting challenges online. Is this actually true?

CRBs rely on automated reinvestigation systems to convert pre-selected challenges into codes sent to furnishers for investigations. The creditor may just check the dispute codes against their digital records that originally contained the inaccurate data. With custom letters, the dispute process is more personalized. Still, CRBs must remove late payments from your credit reports as long as they are inaccurate. If the first challenge fails, you can file a redispute.

3. Ask creditors to remove inaccuracies directly

Section 623 of the FCRA specifies that furnishers have a duty to correct and update inaccurate information. This gives customers the power to ask creditors to remove errors from their credit history.

The letter used to request removals from furnishers goes by the code “623”. Customers can still notify the customer support team and request information on how to report the mistake. Sometimes a call or email is enough. After investigations, furnishers should notify the CRBs promptly and recommend the relevant corrections.

Is it easier to deal with the lender only? The National Consumer Law Center asks consumers to submit disputes with all involved parties. Dealing with furnishers only robs consumers of the right to seek legal relief if the lender mishandles their case.

Various consumer redress options are available if CRBs mishandle the case. Consumers can bring lawsuits or launch complaints with the Consumer Financial Protection Bureau (CFPB).

If you decide to write an email or letter to the furnisher, you can’t go wrong by adding the following details:

Identifiable information;

Account number if applicable;

Reason for writing;

The dispute in question;

Date of the dispute;

Reason for the challenge;

Attached documents.

Lenders may not pull your reports to analyze entries. Attach your report as a PDF along with other supporting documents such as account statements.

You can also use the following CFPB sample letter for disputing information by mail. The agency recommends requesting a return receipt as evidence of the delivery.

4. Petition for Goodwill removals

It’s not illegal for creditors to remove delinquency from a report even if the information is true. Customers just need to request a goodwill adjustment. Basically, it entails writing a letter or email explaining the reasons for the late payment. In the request, you ask for forgiveness.

The method of getting late payments removed has a higher probability of working if:

Your reasons are genuine and backed by evidence;

You had a nice relationship with the lender with no other incidences of late payments.

Now, not all lenders may honor a request to remove accurate late payments on credit reports. CRBs ask data furnishers to avoid altering genuine entries. If the CRB suspects any misconduct from the lender, they may revoke their right to supply information.

There is good news. Deleting late payments from your credit may not be on the top list of punishable offenses. CRBs hugely frown upon the practice of re-aging debts where lenders change the date on a delinquent account to make it stay on the report for longer. The practice also interferes with the Statute of Limitations for debts, making it highly illegal.

Make your case to someone with the right authority for a Goodwill adjustment request to have a higher chance of success. You may need to contact customer support and ask for the decision-maker. They may be willing to help. Sending a goodwill letter without guidance on who to contact is not likely to work.

You may receive notification to write a late payment letter. Keep it original, offer genuine reasons, and show how you plan to avoid delinquencies. Again, there are no assurances of this method working, but it’s worth a try.

5. Remove late payments due to Covid-19

Top lenders and card companies have announced various measures to relieve the impact of the pandemic on their customers. Capital One has a dedicated page where customers can ask for assistance if they have trouble making their monthly payments. The Federal Student Aid suspended loan payments, collection attempts and applied a temporary 0% interest rate for Ed-owned federal loans.

Some lenders have stopped reporting late payments and will waiver late payment penalties. Customers also have certain rights under the Coronavirus Aid Relief and Economic Security Act (CARES). It contains provisions for the forbearance of various types of loans, including mortgages and student loans.

You should speak to your lender to see if they can help remove delinquencies due to covid-19. It’s also important to keep other accounts from becoming delinquent by contacting creditors beforehand. Many financial and non-financial institutions have stepped up to offer relief and may provide help meeting other bills.

6. Negotiate for removals with a pay for delete letter

A pay for delete letter is another strategy for negotiating the removal of a missed payment on a credit report. It’s a two-way street. You offer to pay the debt in full or set up automatic debits from your bank account. In return, the creditor removes the late payments. Customers may also make other requests, for instance, asking the collector to change the account status from settled to paid in full.

Is it possible to have an account in collections removed? It will be a big ask compared to deleting late payments or changing the account status and may raise suspicions of report manipulation by the three major credit bureaus. Creditors may turn down pay for delete offers initially, but it never hurts to ask again.

Should You Hire a Credit Repair Company to Remove Late Payments?

Credit repair companies have a wealth of experience garnered from helping thousands of customers identify and resolve difficult issues. They ease the repair process by handling all communications by CRBs and creditors.

All reputable companies work with trained experts who may be more adept at spotting credit issues. They understand the procedures for reporting errors that companies must follow. You also receive guidance on information or evidence you’re entitled to request from creditors and credit bureaus.

A company such as Lexington Law may provide legal help as their team consists of attorneys. If there is a need to seek redress for mishandled disputes, they can advise on viable legal challenges.

Repair companies include extra services as part of their packages, for instance:

Regular score and report updates;

Assistance in sending debt validation or goodwill letters;

Credit rebuilding guidance and advice on rebuilding products;

Lender or employer recommendations.

Ovation Credit Repair sends recommendation letters to future lenders for customers applying for credit products with bad credit. Their word carries weight as the service is part of LendingTree, the largest online loan marketplace.

Arrive at the final decision to hire a credit repair company after considering your finances. On average, customers pay about $79 per month plus an initial fee. There’s nothing that paid companies can achieve that you can’t replicate yourself, but they certainly make the process less cumbersome for many consumers.

How Long do Late Payments Stay on Credit Reports?

If all attempts to remove late payments on credit cards fail, don’t fret! The FCRA governs the length of time negative entries can remain on reports. Most negative marks stay for seven years, such as late payments, foreclosures, collection accounts, and Chapter 13 bankruptcies. Paid-in full and closed accounts in good standing have a longer shelf life of up to 10 years.

If records of an active account contain a late payment that is seven years old, you can dispute the entry with the CRBs.

As you wait for the negative entry to fall off, you may need to apply for credit products, and lenders will review your reports. Credit Reporting Bureaus allow customers to add statements to explain various negative entries. The statements don’t affect scores, but they can offer context to potential lenders, landlords, or employers. You can inquire about adding consumers’ statements by contacting each customer support team.

Do Late Payments Affect Credit Scores?

Late payments fall into different categories depending on how long they have been overdue. Payments may be 30, 60, 90, 120, or 150 days late. After 180 days, most lenders will charge off the accounts or write them off as losses. The longer the delinquency, the greater its impact on scores, but its effect diminishes as it ages. WalletHub states that delinquencies only impact scores for the first 12 to 18 months.

Credit reports are unique, and not all customers will take a big hit following a late payment entry. FICO published various case scenarios illustrating the impact of late payments on credit scores. In one case, they illustrate that a homeowner aged 43 years with a FICO score of 736, a credit utilization rate of 20%, the revolving balance of $20,500, 25-year history, and no recent delinquencies may see their score dropping to 685-705 following a single missed payment of 30 days.

If they miss a payment by 90 days, their scores may decrease to 655-675. The Damage Impact Assessment further showed that people with lower scores tend to experience a lower reduction. Customers with a short credit history and good scores may experience a huge drop in scores than more experienced borrowers.

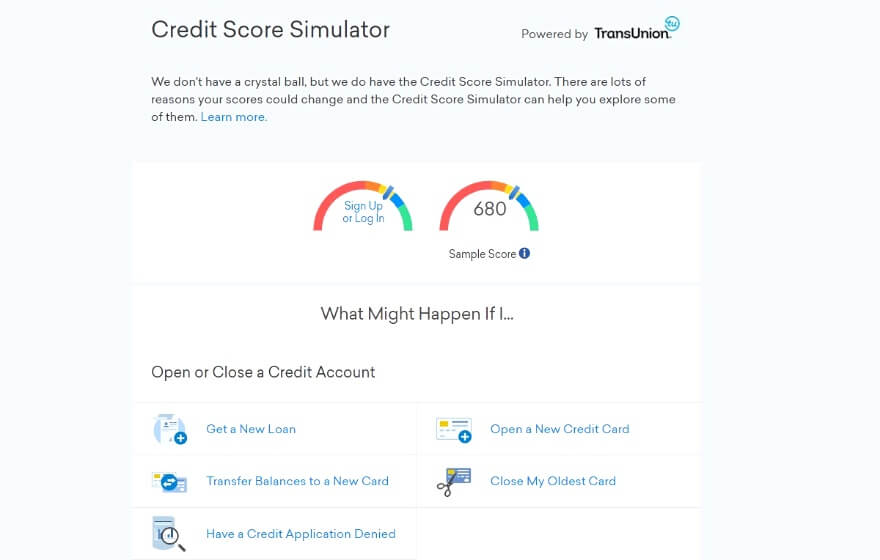

You can check out their report for more scenarios. Alternatively, you can use credit score simulators such as the Credit Karma simulator. It shows the real-time impact of positive and negative entries.

Be very careful about co-signing loans. You may agree to boost someone’s chance of qualifying for credit, and they will assume responsibility for handling the loan repayments. However, missed payments may affect your payment history.

Bottom Line

It’s possible to remove a late payment from credit reports without the intervention of paid services. Challenge the CRBs by filing a dispute and also dispute the error with the original creditor.

Lenders forgive genuine late payments for customers with good track records. Various credit relief options have also become available to lessen the impact of the pandemic. Finally, consider hiring a paid credit repair company for a much smoother repair process, but only if your budget allows it.

Ricky Ingram

Founder of Credit Repair Partner. I worked in the credit repair industry for about 10 years. I love, helping people become smarter about their credit and finances.

Have you recently received a letter from LVNV Funding LLC? LVNV Funding is a debt collection agency that purchases debt from creditors all over the country and then attempts to collect it. This may be due to a past debt that you have associated with one of your credit lines. The situation can be confusing...

Has the CBC Group recently reached out to you? Or have you received a statement for outstanding medical bills, utilities, and other accounts?

Get Help With Late Payments!

(877) 324-2390

Free Consultation

If you’re currently dealing with a...

A 633 credit score is considered slightly below average and is categorized in the “fair credit score” group. Despite the fact that you are not in the poor score category, there is still so much room for growth, and you should take advantage of it. Think of your score as a stepping stone to bigger...

A 619 credit score is a fair credit score, putting you side by side with the average American. It is not a bad score, but it is also not excellent. When lenders see a 619 FICO score they will most likely not show an unwillingness to work with you, but they will end up giving you higher interest rates....

A 627 credit score is something to work on and improve as it falls into the fair credit score range. Consumers in this category may be regarded as subprime borrowers. They statistically have a higher rate of becoming delinquent than borrowers in higher credit score categories.

The impact of poor scores...

Millions of Americans struggle with their credit scores. The best credit repair software can provide you with the resources to help you in the process. Credit is not an easy topic to navigate, and making small mistakes can drastically hurt your score. When it comes to the importance of keeping a high...

Founder of Credit Repair Partner. I worked in the credit repair industry for about 10 years. I love, helping people become smarter about their credit and finances.