How to Remove Student Loans from Your Credit Report?

How to Remove Student Loans from Your Credit Report?

Published by: Ricky Ingram

Disclaimer: We provide free content for our users. But, we can earn commissions when you click on affiliate links to one or more of our advertisers. Learn more about how we make money.

These days, it’s normal for a bachelor’s degree to cost $240,000 or more. The sad reality is that most people cannot afford this, and end up having to take out loans to pay for part or all of their education. If you need a loan to pursue your education, then it’s crucial that you know about removing student loans from your credit report. Your predicament will cause enough headaches as is — you don’t need to add having a bad credit score on top of it all.

Wondering what forms these loans come in, or how they might impact your financial standing during and after school? This article will walk you through everything you need to know about giving yourself the best possible chance at removing student loans from your credit report. Note that only mistakes are actually removable. If you have failed to be a responsible loan manager, then attempting to have bad marks removed from your report is likely not worth your time. In this case, there are better routes for you to take described below.

Read on to learn about how credit bureaus perceive your loans and what you can do about it.

Once you have determined that you have no choice but to take out a loan to fund the degree you seek, you have two main options. You can acquire private student loans. These come with all types of nuanced contingencies though and may prove to be more of a hassle than they are worth later on. The alternative (and arguably safer option) is to obtain a federal student loan, which comes in four different varieties:

Subsidized — Your eligibility is based on need and status as an undergraduate student;

Unsubsidized — Status as a higher-education student is still required, but it is not based on economic need;

PLUS – These are available to (a) graduate and professional students or (b) the legal guardian of a dependent undergraduate. They exist to cover expenses that are otherwise uncovered by aid; and

Consolidation — This lets you combine all of the loans you have taken into one sum with a single loan servicer (a type of debt consolidation).

Most of these federal routes do not require pulls on your credit to determine whether you have sufficient standing to receive assistance. The big exception to this is the PLUS option. A demonstration of need is not required for this option, but you will have to go through the credit check process to prove eligibility for PLUS. Having a substandard credit history is not always a nail in the coffin if this is the route you need to take. However, it will make obtaining a PLUS more difficult, requiring you to meet additional standards if it does not bar you altogether.

If you have a federal student loan closed on your credit report, you may be interested in knowing how long it will be there. It’s important to note that federal student loans fall under the installment category and are therefore treated like other installment loans. Lendings that are academic in nature do not get special treatment.

How to Get Student Loans Off a Credit Report?

Depending on whether you are the holder of a government or private loan, the methods for getting student loans off your credit report are going to vary. If you are a private holder, then your options are significantly more limited. Ultimately, it will come down to the details of your contract. You usually need to show the cases of extreme hardship to get bad marks off of your payment history.

If you went the government route, you are in a better position. While not all student loans on your credit report can be removed, there are a variety of categories that can be. Here are some examples:

If you did not actually take the amount out, and it is in your account accidentally.

If your account fails to reflect a successful pleading of forbearance or deferment.

If you already engaged in fixing defaulted student loans, and your institution failed to update your account to show this.

These are some common corrections that can be made, but it is not exhaustive. A good rule of thumb is as follows: If you are attempting to correct a mistake made by the credit bureaus, your bank account, or another third party, it is worth your time and effort to try to get it corrected. However, if the information you are attempting to challenge is genuinely your fault, there probably isn’t much you can do. Removing late student loan payments is not usually possible unless there has been a misunderstanding or mistake.

How Long Do Student Loans Stay on Your Credit Report?

Do student loans fall off your credit report? They can. Will it be a painless process? Unfortunately not. Once you have been considered to default, this information gets passed along to the major credit bureaus as something called a “collection.” Should you pay off the amount, your status will change to “paid.” However, even after you pay in full, the mark will, unfortunately, remain on your credit report. Usually, student loans are removed after 7 years.

If you never completely pay them off, delinquent student loans are unfortunately very stubborn. People sometimes joke that they follow you beyond the grave. In some instances — for example, if your loan is private — this can be true. However, if it was a loan from a government program, then it will be dissolved, or “forgiven,” after your passing. Some administrations have invented ways for forgiveness while you are still living as well. If you think you will not be able to avoid defaulting, even after loan refinancing, or you won’t be able to pay off your monthly payment due to interest rates, this is probably your best option.

How Do Student Loans Affect Credit Scores?

Just because your circumstances have forced you to take out a loan does not mean that you have to give up your good credit. Although credit bureaus do not release all of the details about how your score is formulated, they do provide some helpful insight into the process. Loans fall into the debt category of your score, which often makes up between 15% and 40% of your score. It is possible for you to owe a five-figure sum to a public or private institution and still have an excellent score on your credit report.

What matters most is your payment history. So long as you are paying off what you owe in a timely manner and in the correct amounts, having student loans on your credit report shouldn’t affect your score. It’s untimely payments that can do the real damage. Payment timeliness makes up between a fourth and a third of your score. Thus, just one month of delinquency can knock you down nearly 100 points.

How to Dispute Student Loans?

Unlike most things in the credit world, disputing is fairly formulaic. First, you will want to obtain a free credit report. Then, you should skim the report to see if you notice any incorrect information. You can do this on your own if you are familiar with the document, or you can seek professional assistance.

If you do find something you believe to be an error, then you will want to begin the dispute process by drafting a letter. The letter should contain your personal information, the error you believe you have found, and most importantly, evidence proving that it is, in fact, an error. If you fail to provide persuasive evidence, your challenge will fail. Then, you can upload or mail your letter.

It typically takes about a month to hear back about your challenge. If it is approved, then the mistake will be corrected, and your score should reflect this correction by increasing.

Sample Student Loan Dispute Letter

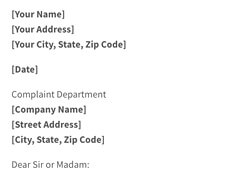

The Federal Trade Commission (FTC) has conveniently provided a guide to follow when drafting a dispute letter. While this is not specifically for a student loan dispute letter, it will work for challenging any discrepancies. You should begin your letter by cultivating a neat and simple header containing your information, the credit reporting agency’s information (or other entity you are addressing the letter to), and a formal opening, as pictured below.

If you want, you can also include a subject line, such as “late student loan payment removed from the credit report.”

Then, if you can locate your loan number, it is helpful to add this number at the beginning of your letter. After identifying the loan you are attempting to challenge, you will want to state your reason for the challenge. This could be as simple as saying, “My statement indicates that I have made a late payment when in fact, I have paid all of my statements on time and my loan is not currently defaulted.” Almost any issue can be plugged into the formula below.

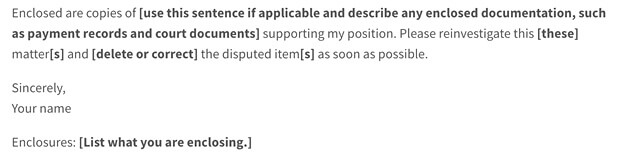

After stating your reason for the challenge, you’ll want to back it up with as much evidence as is required to prove your point. In addition to describing this evidence in your goodwill letter for your student loan, you should also include copies of documents backing up your statement. There’s no such thing as too much tangible proof! Then, respectfully sign your communication and indicate what the reader should find enclosed in your challenge.

You should also have your letter proofread. If you have not retained the assistance of a credit specialization company, then have it proofread by an educated person you trust. Also, resist the urge to use an impolite tone or demand that your account be mended immediately.

The person who will read your letter is not the one who made the initial mistake, but they are in charge of determining whether your dispute will be accepted. It typically takes up to 30 days for your dispute to be reviewed, so try to exercise patience during this time.

Need Help Considering Your Options?

Whether you are attempting to remove transferred student loans from your credit report or to correct a mistakenly applied missed payment, a goodwill letter can go a long way toward preserving your credit. Sending a company such as Navient a goodwill letter cannot hurt, and hopefully, it will help you in your journey to credit or student loan repair.

Are you feeling overwhelmed about going through the process described above? You’re not alone. Nearly 80% of Americans have accumulated some type of debt during their lifetime. This can be a daunting predicament to get out of for any layperson. Fortunately, there are credit repair companies that can sit down with you, help you analyze your options, or even take care of the problem for you!

Some of the best repair companies are listed below.

Whether you choose to pursue your loan journey on your own or with professional help, know that you do not have to fall victim to a poor score just because you have student loans. It is possible for you to have loans and still be seen favorably by the credit bureaus.

Ricky Ingram

Founder of Credit Repair Partner. I worked in the credit repair industry for about 10 years. I love, helping people become smarter about their credit and finances.

Have you recently received a letter from LVNV Funding LLC? LVNV Funding is a debt collection agency that purchases debt from creditors all over the country and then attempts to collect it. This may be due to a past debt that you have associated with one of your credit lines. The situation can be confusing...

Has the CBC Group recently reached out to you? Or have you received a statement for outstanding medical bills, utilities, and other accounts?

Get Help With Late Payments!

(877) 324-2390

Free Consultation

If you’re currently dealing with a...

A 633 credit score is considered slightly below average and is categorized in the “fair credit score” group. Despite the fact that you are not in the poor score category, there is still so much room for growth, and you should take advantage of it. Think of your score as a stepping stone to bigger...

A 619 credit score is a fair credit score, putting you side by side with the average American. It is not a bad score, but it is also not excellent. When lenders see a 619 FICO score they will most likely not show an unwillingness to work with you, but they will end up giving you higher interest rates....

A 627 credit score is something to work on and improve as it falls into the fair credit score range. Consumers in this category may be regarded as subprime borrowers. They statistically have a higher rate of becoming delinquent than borrowers in higher credit score categories.

The impact of poor scores...

Millions of Americans struggle with their credit scores. The best credit repair software can provide you with the resources to help you in the process. Credit is not an easy topic to navigate, and making small mistakes can drastically hurt your score. When it comes to the importance of keeping a high...

Founder of Credit Repair Partner. I worked in the credit repair industry for about 10 years. I love, helping people become smarter about their credit and finances.