Disclaimer: We provide free content for our users. But, we can earn commissions when you click on affiliate links to one or more of our advertisers. Learn more about how we make money.

They say shoot for the moon, and if you miss, you’ll hopefully land on the stars. It’s the perfect advice to give anyone who wants to pursue an 800 credit score.

So, what qualifies as the moon? Well, it’s an 850-credit score, the highest score you can ever achieve and the epitome of credit success.

The rationale is, if you adopt habits that can get you a perfect score, you may well find yourself with a FICO score of 800. Trying to improve a poor credit score and, at the same time aiming to achieve an exceptional credit score may seem improbable.

You may be surprised to learn that the percentage of the population with a credit score over 800 stands at about 20%. Those are millions and millions of people with exceptional credit.

You may become part of the 800 Club by following simple rules as recommended by CreditRepairPartner experts. First, though, let’s start by looking at what a near-perfect credit score can get you:

Good jobs, lavish apartments, and enormous rewards points on plastic cards are the attractive benefits of a credit score over 800.

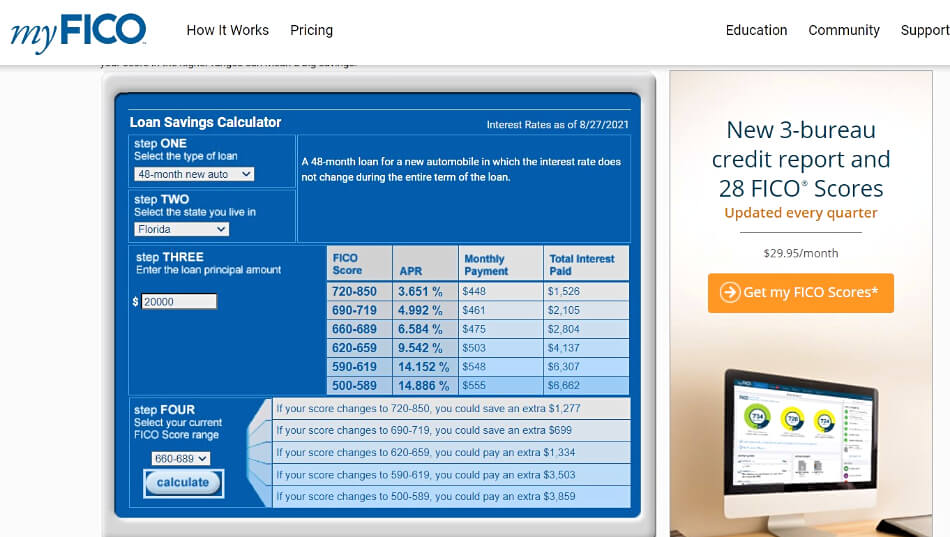

As an exercise to find out how much you may save with a high credit score, we recommend using a loan saving estimator to compare rates on loans:

For instance, the myFICO Loans Saving Calculator discloses that you may save up to $1,277 by improving your scores from 660-689 to 720-850.

There’s another little benefit of having an 800 credit score. You’ll enjoy exclusive bragging rights unless you also know someone more exceptional.

How to get a credit score over 800?

Are you eager to improve your credit score? There is something you should know. Your score is taken as a measure of your creditworthiness. It doesn’t carry a positive connotation. It’s actually how less likely you are to default on a loan within 90 days.

Credit scores are measures of risk intended for use by lenders to help mitigate losses from bad loans. Scoring companies keep updating their credit prediction models to make them better at gauging risk. That’s why you have the hugely popular FICO Score® 8 and its new cousins, FICO® Score 9 & Score 10.

Certain risk factors may make you less likely to default on a credit card, and they may differ from factors that may cause you to default on an auto loan.

Scoring companies like FICO publish industry-specific scoring models. That’s why if you’re getting your score from different lenders, it may have some variations. What’s more, it may be based on the VantageScore model, which is a bit different from FICO.

Consumers with exceptional scores (800-850) only have a 1% risk of becoming delinquent on new credit lines. How do you become less of a credit risk:

Step 1: Maintain a spotless record

If you want to have exceptional credit, you must demonstrate near infallibility when it comes to racking up negative items.

Your listed accounts must absolutely not have negative items such as late payments. For instance, if you have had a credit card open for the last five years, it must have a perfect history, with no exceptions.

Here is a valid question you may ask, “But what if I already have an account with a payment history stained with derogatory entries?”

Negative entries don’t go on your permanent record. Credit bureaus delete most negative marks after they have aged for at least seven years. It gives you a chance to start over.

If you want to attain an 800 credit score after bankruptcy, you may need to wait for seven years for Chapter 13 bankruptcies to be removed and 10 years for Chapter 7 bankruptcies to fall off your reports.

Step 2: Maintain near-zero balances on revolving credit accounts

This is a drastic recommendation. You can take it with a grain of salt, but it’s actually founded on real insights.

When Experian revealed the traits of consumers with perfect scores, they discovered that they owed an average of $3,025 on plastic card debt, which was half the national average.

Are borrowers with perfect credit not supposed to receive higher credit limits? Yes, they receive the highest limits, but they maintain very low credit utilization rates. Ideally, shoot for an average CUR across your revolving credit accounts of less than 10%. Keep in mind that the CUR makes up to 30% of your FICO score.

For instance, if you have a total of $70,000 available in credit, your outstanding balances at the end of the month should be $7,000. If it’s near zero, all the better!

“Will I need a high income to get an 800 credit score?“ No. While there may be a correlation between high incomes and perfect credit, you don’t need a high income.

Based on Experian Q4 data for 2018, about 11.49% of people with scores of 850 had annual incomes of about $25K – $50K.

Step 3: Length of credit

The credit age contributes 15% during score calculation. It’s defined as the length of time you have had certain accounts open.

Baby boomers are more likely to have perfect credit compared to millennials and Generation Y. That’s because older people tend to have aged accounts. A LendingTree study featuring over 100,000 user accounts established that most people in the 800 credit score club had an average credit age of 22 years.

It’s not all bad news for young people. Up to 4% of millennials and 1% of Generation Y had perfect 850-scores in 2018.

If you’re looking for a way on how to increase your credit score to 800, you should avoid closing older accounts.

“Should I simply leave an account open for it to age?” The FICO® scoring model looks at the ages of specific accounts, average age, and how long you have used certain accounts. Leaving an account open without using it may not provide the boost you need.

If you keep your revolving accounts open, make sure they are active by only making minimum purchases and pay off the balances in full.

Step 4: Establish a healthy credit mix

How many credit accounts do you have open? The LendingTree study established that people with perfect credit had an average of 7.9 active accounts. You’re not going to raise your credit score to 800 by only having credit card accounts. It’s prudent to obtain other credit lines such as auto loans, mortgages, or personal loans.

Step 5: Limit your credit applications

In an attempt to reduce the credit utilization rate, some customers will happily apply for new credit cards. There is no fault with pursuing new credit but do it cautiously. Every time you are approved for a loan, the lender has to conduct a hard pull. Hard inquiries may reduce your scores by a few points.

According to the LendingTree analysis, people with credit scores of over 800 averaged not more than 2.8 hard inquiries within the last two years. Ideally, you should limit yourself to about one or two hard inquiries per year.

Step 6: Get a boost from a family member or friend

You deserve to get a helping hand when you’re trying to achieve the best FICO score range. There is no better way to do this than becoming an authorized user or someone else’s credit account.

It’s a strategy that has paid off for parents who have added their children as authorized users on their credit card accounts. You may find a teenager with an average credit history of 10 years while never applying for new credit.

Bonus Tip: Dispute credit errors

You should keep an eye on your credit reports to ascertain that they are error-free. Material errors such as collections accounts can significantly reduce your credit score.

There’s no accurate way to estimate how long it may take to raise your score to 800. However, we can make several guesses. If you already have an excellent score, adopting better credit habits such as maintaining a very low utilization rate may move you one step closer to an exceptional credit rating.

If you’re still young (under 35 years), you may need to continue building up your credit and increasing the average age of your accounts until you’re in a position to be rewarded with exceptional credit.

Don’t stress about the best ways on how to get an 800 credit score. You may enjoy all the benefits of an exceptional credit if your score is over 720, considered excellent. That’s quite attainable as the average score nationwide stood at 711 as of 2020.

Conclusion

There’s no denying that 800 is a good credit score. You can achieve this high rating through a combination of techniques such as paying down credit card debt, avoiding many new credit applications, maintaining a healthy credit mix, and reviewing your reports for errors.

As you search for the best way to get an 800 credit score, avoid scammers that may claim to offer cure-alls for bad credit. They may take your money or land you in legal trouble if they use illegal credit techniques such as using Credit Private Numbers.

Ricky Ingram

Founder of Credit Repair Partner. I worked in the credit repair industry for about 10 years. I love, helping people become smarter about their credit and finances.

A 633 credit score is considered slightly below average and is categorized in the “fair credit score” group. Despite the fact that you are not in the poor score category, there is still so much room for growth, and you should take advantage of it. Think of your score as a stepping stone to bigger...

A 619 credit score is a fair credit score, putting you side by side with the average American. It is not a bad score, but it is also not excellent. When lenders see a 619 FICO score they will most likely not show an unwillingness to work with you, but they will end up giving you higher interest rates....

A 627 credit score is something to work on and improve as it falls into the fair credit score range. Consumers in this category may be regarded as subprime borrowers. They statistically have a higher rate of becoming delinquent than borrowers in higher credit score categories.

The impact of poor scores...

A 626 credit score firmly puts you in the fair score category. That’s according to credit score ranges provided by myfico.com, the consumer division of the Fair Isaac Corporation (FICO).

You may have heard of FICO scores, but some lenders use scoring models provided by VantageScore. The VantageScore...

Credit scores typically range between the 300s and the 800s depending on your credit history. A 550 credit score is normally deemed below average. It is not considered good credit, nor is it considered poor credit. It will not guarantee that you will be approved for a loan, but it also is not going to...

A 665 credit score falls into the “Fair” score range. It’s neither good nor bad. Creditors label applicants with fair or poor scores as subprime borrowers. The implication is that they are at a higher risk of defaulting on a new loan.

At-risk borrowers have limited borrowing options. For instance,...

Founder of Credit Repair Partner. I worked in the credit repair industry for about 10 years. I love, helping people become smarter about their credit and finances.