Disclaimer: We provide free content for our users. But, we can earn commissions when you click on affiliate links to one or more of our advertisers. Learn more about how we make money.

Is it possible to improve your credit score in 6 months? Yes, and it is the minimum amount of time required to have at least one account open to generate sufficient credit history to be scorable.

If you are brand new to the credit world, you can apply for your first credit product and continue making payments for the next six months.

What will be the average credit score after the first 6 months? If the account is in good standing, meaning that you have not incurred any negative entries such as a late payment, the score may sit in the 700 range.

If you’re building up your credit after devastating life events such as a job loss, it’s entirely possible to raise your credit score in six months.

This CreditRepairPartner guide focuses on straightforward strategies you can employ. You only need to be motivated.

Before uncovering the various ways to fix credit, it’s essential to know where you stand in terms of your finances and credit rating.

Undoubtedly, your goal to boost your scores may have arisen due to getting denied on a loan. Reading the loan decline letter is a good place to start. The loan underwriter may have disclosed their reasons for rejecting your application.

Some common reasons for rejection include:

Bad credit or low scores: It’s expressed as having a score of 620 or lower. Sometimes the lender’s threshold starts at 679.

High debt-to-income ratio or a large amount of debt: It implies that a large percentage of your income goes towards paying off existing loans and fixed monthly expenses.

An occurrence of many credit inquiries: Lenders may look at the number of hard inquiries within the last six months to gauge the frequency you have been applying for new credit. Six or more hard pulls may be grounds for loan rejection.

Next, request free electronic copies of your credit reports through annualcreditreport.com. If you have used the site before, you may probably know that they only issue a free report from each bureau every 12 months.

That has changed temporarily. The site now offers free weekly reports as part of bureaus’ efforts to alleviate the financial ravages of the pandemic.

The report doesn’t include the score. Actually, credit bureaus and scoring companies are two independent entities.

Scores are not always free, but luckily we have some top places to get free scores without applying for a loan:

Credit bureaus count on the accurate reporting of information furnishers such as public information sources and creditors. To err is human, and that’s why credit reports may contain many mistakes.

Don’t think this can’t happen to you. An average person has about four credit cards and may have opened other credit accounts. With so many accounts, mistakes are bound to happen eventually.

Stay on top of mistakes by combing through your credit reports looking for reporting inaccuracies.

An honest mistake, such as the credit limit on your card being listed as $200 instead of $2,000 may have a considerable effect on your credit utilization rate (CUR). It contributes up to 30% of points during score calculation.

The removal of serious inaccuracies such as collection accounts may even result in a 100 points increase.

You don’t have to do this process alone. The credit repair industry has arisen from the mistakes information furnishers make when reporting data. Companies such as Lexington Law file millions of challenges every year.

You can decide to delegate the work of finding and challenging mistakes to seasoned professionals. Additionally, you can fix your credit report on your own as it’s within your rights to do so.

You may not need paid services in the first place. Take advantage of the free consultations offered by credit firms to ask if they can help.

Step 2: Consider applying for a new credit product

You may ask: “Is it wise to apply for a new loan? I just got rejected!”

Well, it should not be a loan that’s hard to get due to its strict eligibility criteria. Instead, apply for secured credit cards or personal installment loans.

What are secured credit card scores? There may be no score requirements. That’s because the credit products are explicitly designed to help customers raise their scores by helping them demonstrate credit responsibility.

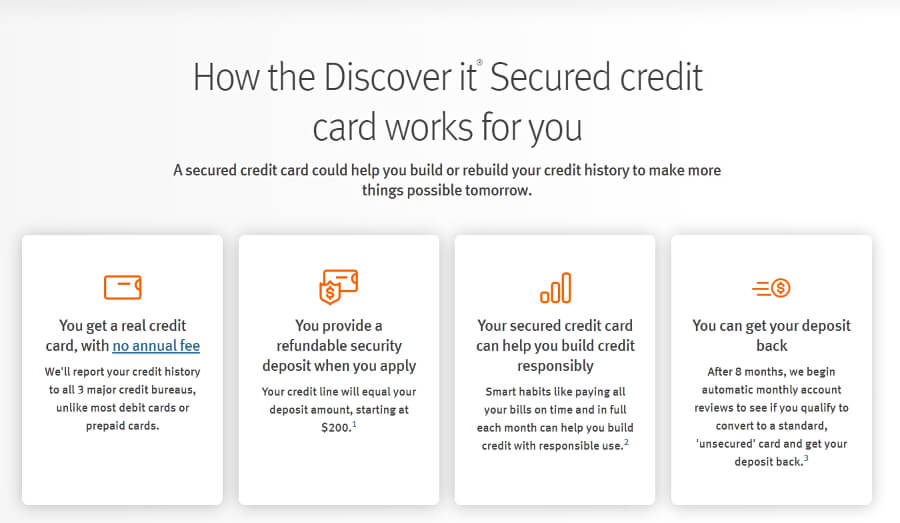

For instance, the Discover it Secured Card comes with no annual fee and includes reporting to the three bureaus. You will need to provide a refundable security deposit that starts at $200. The available credit limit does not exceed the security deposit.

Once you have the card in your hands, you use it reasonably to make small purchases. At the end of the month, you clear the balance and earn points.

Most companies will review the account after 6 or 8 months and refund the security deposit while allowing you to use the card as normal. Contact your card company and ask about their secured card.

This is a powerful way to improve your credit score in 6 months or establish new credit. The only limitation is that you have to provide a security deposit.

Step 3: Improve your CUR by paying down Card Debt

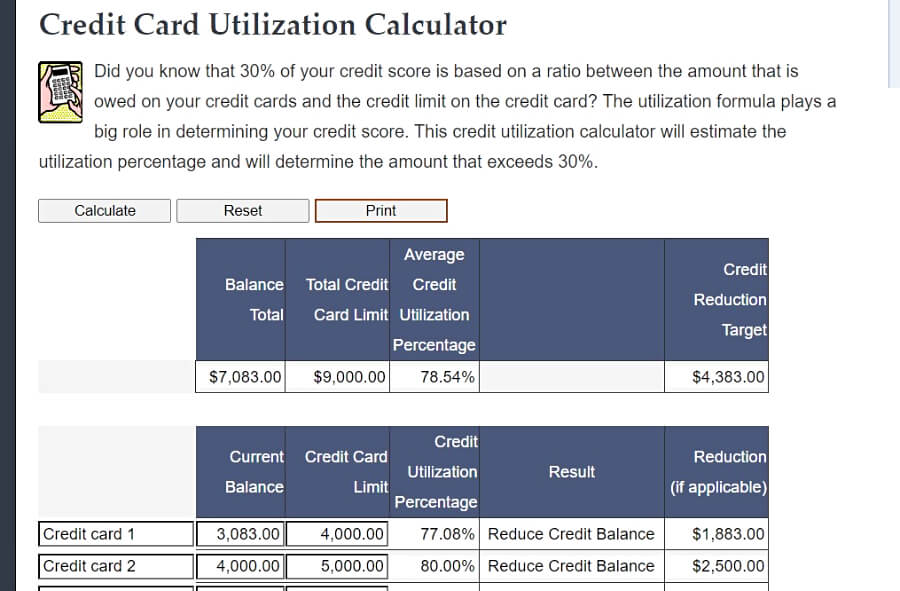

Experts advise that the average CUR should not go over 30%.

We calculate the credit utilization rate using the simple formula:

CUR = (Amount owed on card/Credit limit) x 100%.

If you need to calculate the CUR quickly, use a free calculator. We love this one from AnyTimeEstimate, as it even shows the amount to reduce:

Tip: Check the particulars of your card, such as the limit from your last month’s billing statement.

If you already have a good score, maintaining a very low CUR may get you a 720 credit score in 6 months.

Some experts promote other ways to reduce the CUR, such as:

asking for a credit increase;

or applying for new cards.

Well, consider their advice cautiously, as it is difficult to predict how you may react to a new influx of credit. Many people may choose to spend the extra cash. If you keep racking up more debt, it may erode any progress you may have made in improving your credit score in 6 months.

Step 4: Don’t ignore collection accounts

You can run, but you certainly can’t hide from debt collectors. Rather than trying to outsmart them, focus your efforts on negotiating a settlement or clearing the debt in full.

You may catch a break if the loan company utilizes a scoring model that does not take into account paid collections accounts, such as the newer FICO® Score 9.

Loan companies also avoid approving consumers with unpaid collections accounts as they are a huge liability. For instance, the consumers may be sued anytime and have their wages garnished.

Step 5: Talk to someone about becoming an authorized user (long-term)

Another strategy you can use to improve your credit score in six months is to become an authorized user on someone’s credit card account. It’s the most uncomplicated strategy by far.

Many people are now paying for the privilege to become authorized users, with costs ranging from $150 to $1,500 per month. Tradelines with the highest credit limits and lower CUR fetch the highest prices.

Ideally, you should find someone you know to list you as an AU. It’s not that paying for this service is illegal. When you pay to be listed as AU, you may remain on the account for one or two reporting cycles.

Once you’re removed as an AU, probably after two months, the account ceases to be active on your reports, and its contribution to your scores slowly diminishes before it’s removed after 3 months or so.

However, if you find someone you know, you can ride on their good credit habits for a longer time. Their available credit limit may even reduce your utilization ratio and increase your average credit age.

The strategy is not without risk. If they fail to honor their monthly obligations and incur late payments, you also inherit their mistakes.

Step 6: Report information about your bill payments

Do you pay your bills on time? The self-reporting process entails disclosing additional information about your pattern of bill payments to the credit bureaus.

“Can I report a recent purchase I made?”

All the CRAs allow the inclusion of third-party payment information featuring recurring payments such as:

Monthly rental payments for homes and apartments;

Utility payments;

Streaming service payments;

Telephone bills.

For instance, Experian has made it easy for customers to self-report their payment information through the Boost Program.

Some third-party payment reporting companies such as RentReporters and RentTrack report the alternative credit data for a fee.

Conclusion

As a parting shot, you need to know that it’s possible to raise your credit score in six months considerably.

During your credit repair journey, avoid mistakes that could bring you down. For instance, don’t close old accounts or incur late payments on your student loans. You should also limit your credit applications to avoid racking up hard pulls.

Maybe you’ll not see a big improvement in one or two months. Don’t give up! Stick to your plan, and eventually, you’ll get the score of your dreams and unlock better loan opportunities.

Ricky Ingram

Founder of Credit Repair Partner. I worked in the credit repair industry for about 10 years. I love, helping people become smarter about their credit and finances.

Have you recently received a letter from LVNV Funding LLC? LVNV Funding is a debt collection agency that purchases debt from creditors all over the country and then attempts to collect it. This may be due to a past debt that you have associated with one of your credit lines. The situation can be confusing...

Has the CBC Group recently reached out to you? Or have you received a statement for outstanding medical bills, utilities, and other accounts?

Get Help With Late Payments!

(877) 324-2390

Free Consultation

If you’re currently dealing with a...

A 633 credit score is considered slightly below average and is categorized in the “fair credit score” group. Despite the fact that you are not in the poor score category, there is still so much room for growth, and you should take advantage of it. Think of your score as a stepping stone to bigger...

A 619 credit score is a fair credit score, putting you side by side with the average American. It is not a bad score, but it is also not excellent. When lenders see a 619 FICO score they will most likely not show an unwillingness to work with you, but they will end up giving you higher interest rates....

A 627 credit score is something to work on and improve as it falls into the fair credit score range. Consumers in this category may be regarded as subprime borrowers. They statistically have a higher rate of becoming delinquent than borrowers in higher credit score categories.

The impact of poor scores...

Millions of Americans struggle with their credit scores. The best credit repair software can provide you with the resources to help you in the process. Credit is not an easy topic to navigate, and making small mistakes can drastically hurt your score. When it comes to the importance of keeping a high...

Founder of Credit Repair Partner. I worked in the credit repair industry for about 10 years. I love, helping people become smarter about their credit and finances.