Disclaimer: We provide free content for our users. But, we can earn commissions when you click on affiliate links to one or more of our advertisers. Learn more about how we make money.

A 626 credit score firmly puts you in the fair score category. That’s according to credit score ranges provided by myfico.com, the consumer division of the Fair Isaac Corporation (FICO).

You may have heard of FICO scores, but some lenders use scoring models provided by VantageScore. The VantageScore 3.0 scoring model regards people with a 626 credit score as falling into the poor score category.

What’s clear across the board is that having a 626 FICO score means that you have bad credit, which makes it harder to apply for unsecured cards. Even potential employers and landlords may express an unwillingness to work with you.

You can certainly stress about a credit score of 626. But feeling sorry for yourself is not the best strategy. We will be recommending some of the best techniques to improve your fair credit score.

If you need to borrow a loan right away, you will learn about available loan products for subprime borrowers. Let’s get started:

No, it’s not a good score because lenders will categorize you as a subprime borrower. The title is given to consumers who represent more risk. As a matter of fact, people with scores of 300 to 669 have a 27% chance of defaulting on loan products.

When lenders advance their loans to subprime borrowers, they are not highly certain of getting their money back. For this reason, you will end up paying a higher interest rate to account for the added risk. If you qualify for conventional loan products, the loan amount may be lower.

Credit scores were designed to give lenders a quick overview of your credit behavior and history. So, a 626 credit score has additional meaning. It may infer that you have some past derogatory marks like late payments or collections accounts in your credit history.

Now, how does your score compare with the national average? How does it fit in the overall context? Here are some interesting statistics for your consideration:

The US average FICO credit score in 2020 was 711 (Experian).

Consumers with 300 to 639 scores are likely to have an average credit age of 2.5 years (CreditKarma).

Millennials and the newest generation, Generation Z, are more likely to have a score between 300 to 639 (Credit Karma)

Louisiana had the lowest average credit score in 2020 at 685, while Minnesota had the highest score at 739.

Over 74% of US consumers have scores higher than 626 (Experian).

Credit Cards for a 626 Credit Score

Credit cards for a 629 score are mostly secured. They have a different set of requirements than unsecured cards. The first main requirement is a security deposit. It’s usually about $200 for a new card.

The amount will serve as your available limit. You can’t borrow more than you have deposited typically for the first six months.

If you’re a diligent customer with no repayment issues, the lender may review your account and increase your limit. You will have access to additional credit without making a new deposit.

Will I need to pay interest on a secured card? Yes, and it may range from 18% to 24%. Okay, let’s look at some of the most popular credit cards for 626 credit score:

Secured MasterCard Capital One

The card has a purchase APR of 26.99% variable APR. You don’t pay an annual fee or a transfer fee. New customers can deposit $49, $99, or $200. It also comes with fraud liability protection.

Citi Secured MasterCard

The card is similarly geared at credit rebuilding. You’ll only need to make payments and pay off the balance on time. The secured deposit ranges from $200 to $2,500. The interest rate for the 626 credit score will be 22.49% variable. There is no annual fee and it includes reporting to all the bureaus.

*With a 630 score, some card companies may be willing to offer their unsecured cards.

Car Loan Rates for a 626 Credit Score

There is no average credit score needed for auto loans. You can qualify for a car loan with a 626 credit score. Even traditional lenders such as banks and credit unions may take on the added risk because cars are tangible assets that may be repossessed should the borrower fail to keep up with the payments.

The only caveat is that you’ll end up paying higher interest rates. It’s hard to predict the actual rights unless you submit a new request to get pre-qualified. The process often involves a soft check that will not impact your scores.

Experian’s Automotive insights for Q4 2020 showed that deep-subprime borrowers paid 14.20% on average for auto loans. Additionally, subprime borrowers paid 10.58%, with near-prime consumers paying 6.64% in Q4.

The report summarises the score ranges as:

Deep subprime 300 to 500

Subprime 500-600

Near prime 601-660

Prime 661 – 780

Assuming you had a prime score, you would have only paid an interest rate of 3.69% on average.

Lower monthly payments are not only affordable, but you end up with a car that you can maintain without struggling.

What kind of car loan can I get with a 626 credit score? You may be able to borrow Capital Finance and Credit Union loans. It’s also possible to borrow loans from Buy-here-pay-here car dealerships, but they may have steep interest rates and should be avoided altogether.

Personal Loan for a 626 Credit Score

According to ValuePenguin, the average APR for personal loans for people with scores of 640-679 stood at 22.60% as of April 2021. Interest rates for personal loans cap at 35.99%.

It’s actually quite difficult to find personal loans for a 626 credit score from mainstream lenders. You may need to find alternatives such as working with unions. However, they have membership requirements and may not offer loans before the six-month mark.

If you have available assets such as your car, you may try secured loans. The only disadvantage is that upon failure to repay, you may lose the asset.

Mortgage with a 626 Credit Score

Is a 626 credit score high enough for a mortgage? Yes, it is enough, but not for a conventional mortgage. You may need to look into alternatives for getting a mortgage with a 626 credit score, such as:

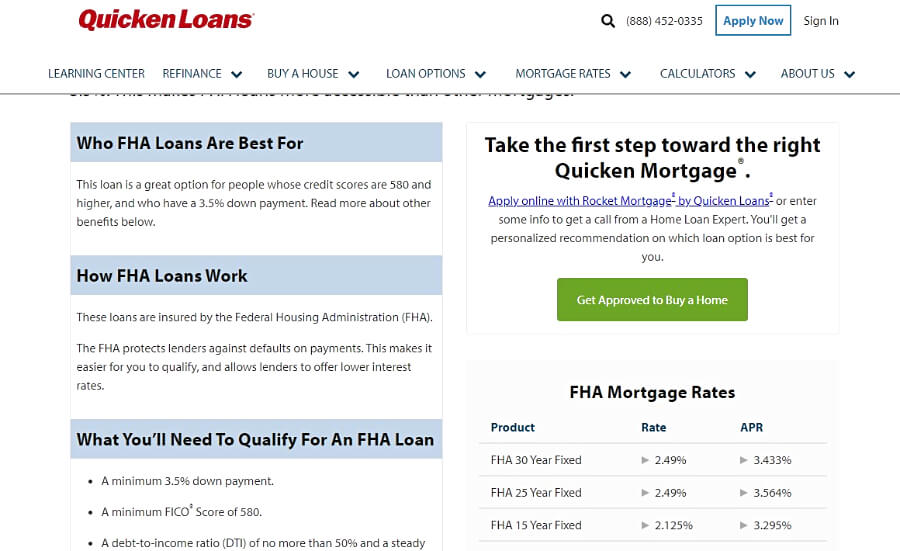

FHA-backed loans: While private lenders underwrite the loans, they are backed by the Federal Housing Administration. You’ll pay a down payment of 3.5% if you have a 580 score or higher. The loans are subject to ceilings each year. For 2021, you can only borrow $822,375 to purchase a single home in high-cost areas and $356,362 for low-cost areas. You can certainly get a home loan with a 626 credit score, but you may contend with extra requirements. For instance, FHA loans require mortgage insurance paid upfront.

VA loan Mortgages: They are geared at helping service members, veterans, and eligible spouses purchase their next homes or conduct repairs. The loans have competitive interest rates, and most lenders impose a 620 score rule.

Single-family housing guaranteed loan program: If your household has a low to medium income and lives in rural areas, you may be eligible for a loan by the USDA. But you may need to bump up your score to at least 640.

*You can check actual FHA mortgage rates from lenders such as U.S. Bank or Quicken Loans.

How to Improve a 626 Credit Score?

You’ll be better off with a good or excellent rating. Even if it takes a couple of months or years to achieve your goal, the wait will be worth it, as you could potentially save thousands of dollars by avoiding high-interest rates.

Let’s look at some of the best improvement strategies, as well as techniques to get a quick boost.

Best long-term credit improvement strategies

Apply for credit rebuilding products such as secured personal loans or cards;

Apply for store cards with monthly reporting to the bureaus—make purchases and pay your balance on time;

Gradually reduce your credit utilization rate across your active cards —simply pay down your balance until you owe very little;

Resolve outstanding collection accounts by asking for a settlement or paying off the balance in full.

Strategies to get a quick credit boost

Approach someone you know and ask them to add you as an authorized user on their card —the account should have a high limit and a spotless payment history.

If you don’t know someone to add you as an authorized user, you can also purchase AU accounts for 2 to 3 reporting cycles from reputable vendors.

Add information about your streaming payments, utility bills, and rental payments through programs such as Experian Boost or RentReporters.

Avoid closing down old accounts that are in good standing.

Pay down your card debt.

Work with a credit repair company to clean up your reports, get credit help, and remove errors. Note that you can also challenge the credit bureaus by yourself.

Conclusion

It’s pretty much possible to get a loan with a 626 credit score. However, lenders will take a close look at your finances when you are applying with bad credit.

Applying for a loan and waiting to see if you’re approved is not a good strategy. Multiple loan applications during this difficult period may result in hard inquiries that will further worsen your scores.

As a recommendation, limit your loan applications that involve a hard inquiry for approval to 2 to 4 per year. You should also constantly monitor your credit report for reporting errors and have them resolved right away.

Ricky Ingram

Founder of Credit Repair Partner. I worked in the credit repair industry for about 10 years. I love, helping people become smarter about their credit and finances.

A 633 credit score is considered slightly below average and is categorized in the “fair credit score” group. Despite the fact that you are not in the poor score category, there is still so much room for growth, and you should take advantage of it. Think of your score as a stepping stone to bigger...

A 619 credit score is a fair credit score, putting you side by side with the average American. It is not a bad score, but it is also not excellent. When lenders see a 619 FICO score they will most likely not show an unwillingness to work with you, but they will end up giving you higher interest rates....

A 627 credit score is something to work on and improve as it falls into the fair credit score range. Consumers in this category may be regarded as subprime borrowers. They statistically have a higher rate of becoming delinquent than borrowers in higher credit score categories.

The impact of poor scores...

A 626 credit score firmly puts you in the fair score category. That’s according to credit score ranges provided by myfico.com, the consumer division of the Fair Isaac Corporation (FICO).

You may have heard of FICO scores, but some lenders use scoring models provided by VantageScore. The VantageScore...

Credit scores typically range between the 300s and the 800s depending on your credit history. A 550 credit score is normally deemed below average. It is not considered good credit, nor is it considered poor credit. It will not guarantee that you will be approved for a loan, but it also is not going to...

A 665 credit score falls into the “Fair” score range. It’s neither good nor bad. Creditors label applicants with fair or poor scores as subprime borrowers. The implication is that they are at a higher risk of defaulting on a new loan.

At-risk borrowers have limited borrowing options. For instance,...

Founder of Credit Repair Partner. I worked in the credit repair industry for about 10 years. I love, helping people become smarter about their credit and finances.